Maximizing Social Security

Way Too Important to Screw Up!

Believe or not, Social Security monthly payments make up a huge percentage of most people’s retirement income. The projected benefits for people that have contributed into the system are quite staggering! Note that I said “projected” because the amounts far exceed the expected funds available in the Social Security Trust Fund. This is reason for a little fear that it might not be fully available as promised in the future.

The main reason for this is that so few people are paying into the system compared to those getting a benefit.

This chart illustrates when Social Security was created, 42 people were working for every person that was collecting a benefit. Too bad the collection age was not raised with life expectancy which was 62 when the program was created.

According to the Social Security Administration (SSA) the maximum monthly Social Security benefit that an individual who files a claim for Social Security retirement benefits in 2020 can receive per month is:

$3,790 for someone who files at age 70

$3,011 for someone who files at full retirement age (FRA

$2,265 for someone who files at 62

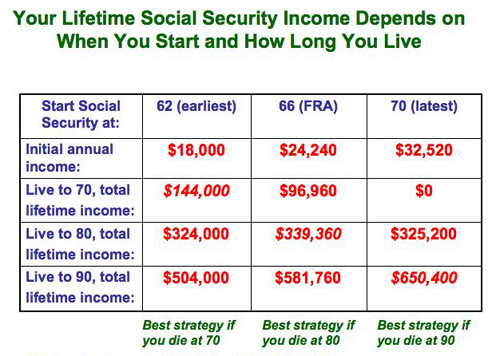

Your Social Security monthly income might go pretty far if you don’t have a mortgage and property taxes are reasonable. Some people unmistakably assume taking your benefit at the earliest age (62) makes the most sense.

While this may be true if you die young, it’s often not the case. Your Social Security monthly benefit increases every year you defer it until age 70. At our firm, we use a calculator that analyzes your benefit to help determine what is the optimal age to turn on your social security monthly payment.

Claiming Age | % Gain from Preceding Year |

62 | na |

63 | 6.7% |

64 | 8.4% |

65 | 7.6% |

66 | 7.2% |

67 | 8.0% |

68 | 7.4% |

69 | 6.9% |

70 | 6.5% |

If you are healthy and have good genes with a long life expectancy, the math will work out in favor of waiting as long as possible to take it.

Click here to find your Social Security Benefit on Government Social Security Website

Social Security Benefits Eligibility & Signup Guide

It’s often not a black and white decision as to when to take your benefit.

CHOOSING TO TAKE SOCIAL SECURITY TOO SOON COULD COST YOU MANY THOUSANDS OF DOLLARS!

One strategy that retirees might benefit from when they first retire and have no income is to covert some portion of their IRA (or 401k rollover) to a Roth IRA while in a low tax bracket. If you need the money to live on from your IRA, you would likely be in a lower tax bracket if you were not also collecting Social Security. It also pushes back the Social Security income benefit which allows it to grow.

There are other retirement income strategies to consider as part of this integral planning decision. Once you apply, you decision sticks, so I’d suggest you get professional advice. I can be reached at 630-942-9007.

Important Points:

Qualifying for Social Security at age 62 requires 10 years of work or 40 work credits.

The maximum monthly Social Security benefit that an individual can receive per month in 2020 is $3,790 for someone who files at age 70.

For someone at full retirement age the maximum amount is $3,011, and for someone aged 62 the maximum amount is $2,265.

How Social Security Works

To qualify for Social Security in the first place requires 40 work credits or approximately 10 years of work.1 If you have 40 work credits, you are eligible to claim Social Security once you reach age 62. The full retirement age, however, depends on the year of your birth.2 For example, if you were born in 1960 or later your FRA is 67; if you were born between 1943 and 1954, it is 66. You can only receive 100% of your benefits if you wait until your FRA to claim. If you claim earlier, you will receive less—and if you claim after age 70, you receive an 8% bonus for each year that you delayed claiming.3

")

")

Leave a Reply

Want to join the discussion?Feel free to contribute!