BETTER HAVE MORE MONEY

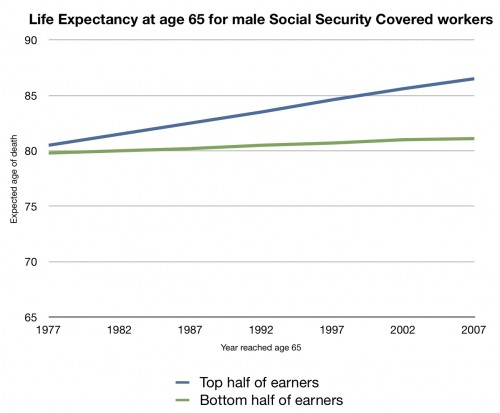

Great news: people are living longer and healthier lives than ever before! Bad news: this means we need more money to allow for those additional years. It would be much easier to plan if we all knew the age at which we would die and worked backward from there. LONGEVITY RISK IS VERY REAL.

As I examine client retirement scenarios, the number one thing we discuss is the income they can afford to take from their portfolio while maintaining a high level of certainty they will not outlive their nest egg. The delicate matter is computing a way for you to spend somewhat freely at the beginning of retirement and then guessing when that spending may start slowing down and by how much.

Not only have medical advances greatly added to expected longevity, but access to high-end care is a major factor in adding to life expectancy. As our society is moving towards a socialist medical system, those that have and can afford access to personalized care will be the ones that will continue to see their life expectancy grow. I routinely run retirement income plans out to age 100 as I believe that there is a good chance that at least one of two spouses will live that long.

If I use my retirement plan as an example and assume my wife dies at age 95 rather than 85, our total retirement spending would grow by over $500,000.

What are some of the best moves you can make to take on Longevity Risk?

1. Plan on working longer. 65 is the new 55 so why not use your energy to continue earning money? Working part-time can make a significant impact on your ability to spend more money in retirement.

2. Move to a low tax state. There is a reason that some states are prone to retirees flocking to them and it’s not just for the weather. Low property and state income taxes can be very attractive, especially when living on a fixed income.

10 Most Tax-Friendly States for Retirees

3. Double up on your savings today. I have seen a fair amount of laziness from pre-retirees as investment returns have been rather high the past few years. You shouldn’t rely on investment returns to be unusually high going forward. The best way to ensure your account balance will grow more rapidly is for you to save more money.

4. Look at your investment portfolio. Many people mistakenly reallocate their retirement money to match their retirement age. This is problematic because you are not withdrawing all your money the day you retire. That money will be invested for your lifetime (joint lifetime if you are married). That could be a 20-40 year investment time horizon.

5. Cost-of Living. Considering #4 above, make sure your portfolio is invested to keep up with your cost of living and at that age, health care may be the biggest future expense.

Longevity Risk is real and most certainly an overlooked risk that retirees face. You shouldn’t wait until you are in your sixties to begin planning for this.

Read about this risk along with many others in our FREE Retirement Report.

Achieving the Balanced Lifestyle:

How You Can Protect, Grow, and Harvest Your Wealth with Comprehensive Retirement Planning

Related Blogs:

")

")

Leave a Reply

Want to join the discussion?Feel free to contribute!