Click on graph to see performance.

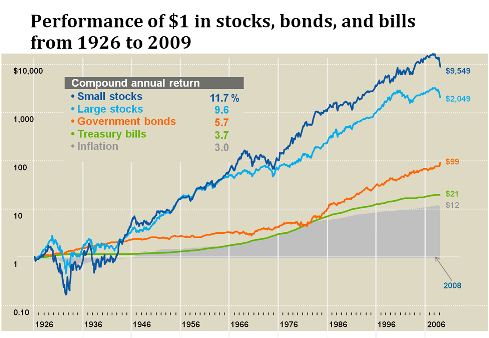

For the past 30 years, interest rates have been moving down and bond prices have been going up. Now, interest rates are at a level when the best case is they “stay flat” as there is not much room to go any lower. With the low-interest rates that bonds offer these days the return proposition on bonds is lower than normal. I cannot get excited about earning three percent or less as the best case scenario for owning many bonds that are available today. I think that a prudent portfolio of stocks could earn 6-9% total return over the next 20 years. This is not a prediction and is based solely on historic returns. Since 1983, I’ve watched the S&P 500 go from about 160 to the 3,100 level it stands today. Despite plenty of bad news and significant declines along the way, that’s a20-bagger!

I say this having no idea which direction the stock market will go in the next few years. Of course, there have been and will continue to be some roller coaster like experiences along the way, but this will not deter me. With retirement money, unlike many people, I look at life expectancy as the barometer for my time horizon, not how many years I have until I retire.

THIS IS ONE OF THE BIGGEST RETIREMENT PLANNING MISTAKES MANY PEOPLE MAKE.

What is the argument for being an investor in bonds?

- Diversification. If you own assets that don’t go down or perhaps go up in value when the stock market drops, it insulates you from some of the pain that goes with being an “owner” of companies. The pain from seeing your account value significantly drop in value could cause you to do the worst possible thing; “sell low”. People that sell low generally never recover. Once you sell low, it’s psychologically difficult to buy back at higher prices. If someone sold their stock mutual fund when the Dow was at 7,000, would they jump back in when it hit 10,000, 12,000, when?

- Safety – Bonds are safe relative to the lendee’s ability to pay the interest owed and return your principle investment when the loan comes due. While you are holding bonds or bond mutual funds the biggest factor regarding their perceived safety is what happens to interest rates after you purchase the bonds or bond mutual fund. If interest rates move down as they have generally done for the past thirty years, bond prices go up, but the opposite happens when interest rates go back up.

I do not anticipate interest rates sky rocketing up any time soon as our government is manipulating the money supply to keep interest rates down for the foreseeable future. Including bonds and other non-stock investments in your portfolio should help to minimize the downside volatility from your stock investments. This ultimately helps protect you from your potential behavior (panicking and selling low).

Paying off Mortgage as Bond Substitute

I have made one significant change in my financial life. I refinanced my mortgage to a 15-year loan. This has become my “fixed income” investment. Normally, I would argue that you are better off taking a 30-year mortgage and investing the difference (you should be able to earn far more than the your mortgage interest rate in a prudent portfolio). I justify using the 15-year loan because 100% of my retirement money is invested in a global portfolio of stocks and stock funds.

If you are living on a fixed income from investments, I sure hope you are not earning 2% on your bond fund or CD and paying 4% on your mortgage ( I bet many people are doing this). If you do refinance, one good idea is to keep the payoff years the same or reduce them if you want to use this as your fixed investment. If you have 22 years to go on your 30 year mortgage, you can refinance and make the new loan for 22 years.

All investments carry some form of risk and that includes bonds. For my clients that own bonds, that risk is minimized by keeping the maturity dates short-term. By doing this, the bond funds greatly reduce their risk if/when interest rates go back up. My clients also tend to have a diversified portfolio of bonds, not just U.S. Treasuries. This reduces risk and helps earn a higher yield.

Contact me if you have questions about your portfolio and would like a 2nd opinion.

Related Posts:

")

Leave a Reply

Want to join the discussion?Feel free to contribute!